Works in Progress Management

|

|

Introduction to Works in Progress Management (WIP)

Works in progress management is based on the accounting principle whereby matching revenues and expenses help determine the moment when costs must be expensed and matched to the revenues they contributed to creating. From a high-level point of view, works in progress management translates to making acounting entries that temporarily move expenses that have not yet been invoiced on the balance sheet OR posting non-invoiced expenses to revenues. That being said, it’s the notion of transferring ownership of produced goods (or services rendered) that determines how works in progress must be accounted for.

When a construction project is completed (or a service rendered) without being purchased by a buyer while it was being built, the organization managing the project must capitalize the construction costs on the balance sheet. These costs are reversed upon the sale, which generally corresponds to the time of invoicing. This is called managing works in progress AS ASSETS.

If, however, the construction project (or service) is transferred to the buyer as it is completed, the costs are posted as expenses; then, at the end of the month, the project’s progress is evaluated to determine the amount that should be invoiced. Afterwards, this amount is used to account for a revenue proportional to incurred costs 1. This is called managing works in progress AS EXPENSES.

Managing WIP in maestro*

Works in progress can be managed as assets (often used by residential construction businesses) or as expenses (used by most organizations). In general, the organization’s management mode, the type of work, the organization’s internal policies, and the invoicing mode determine how works in progress will be managed. No matter which approach is preferred, it must last over time and from year to year. Some organizations use more than one approach depending on the nature of their activities and their projects.

Works in Progress Management Applied to Projects

Maestro* provides the possibility to configure a default works in progress management mode applicable to all projects. It’s also possible, however, to select works in progress management modes specific to projects. In any case, the selected WIP management mode has no impact on project costs.

As Expenses

As mentioned earlier, managing works in progress as expenses means that a project’s costs are systematically posted in expense accounts. At the end of a financial period, an accounting entry is made based on the evaluation and actual use of purchased items or services used; this is done in such a way that expenses represent the real expenses incurred during the period, and a portion of these expenses are deferred to the next period. An income corresponding to the real expenses is obviously accounted for. Some basic maestro* reports, or other reports customized by the customer, can make the task easier and facilitate the estimation of the works in progress amount that is to be used to make the accounting entry and which may or may not be reflected at the project level.

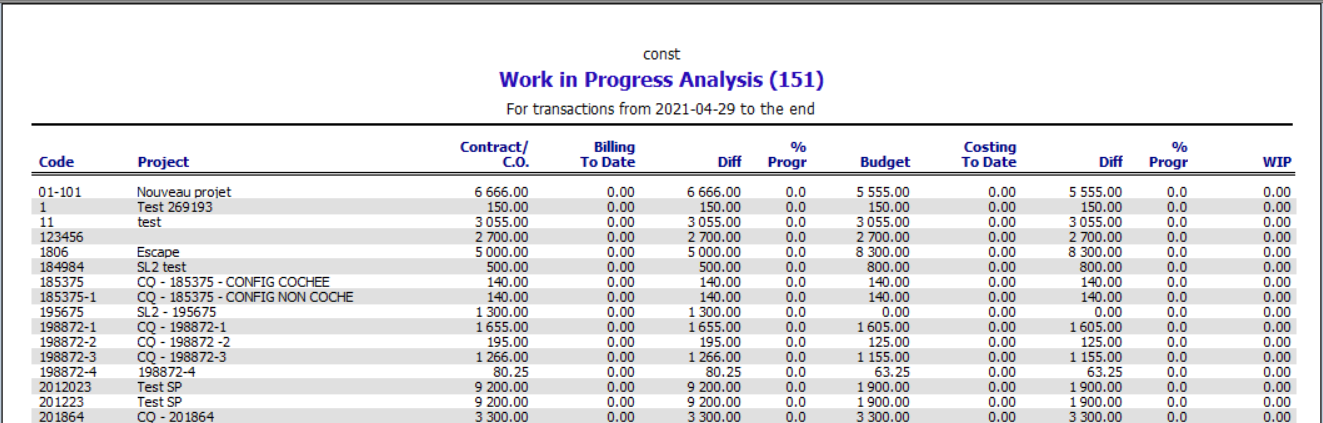

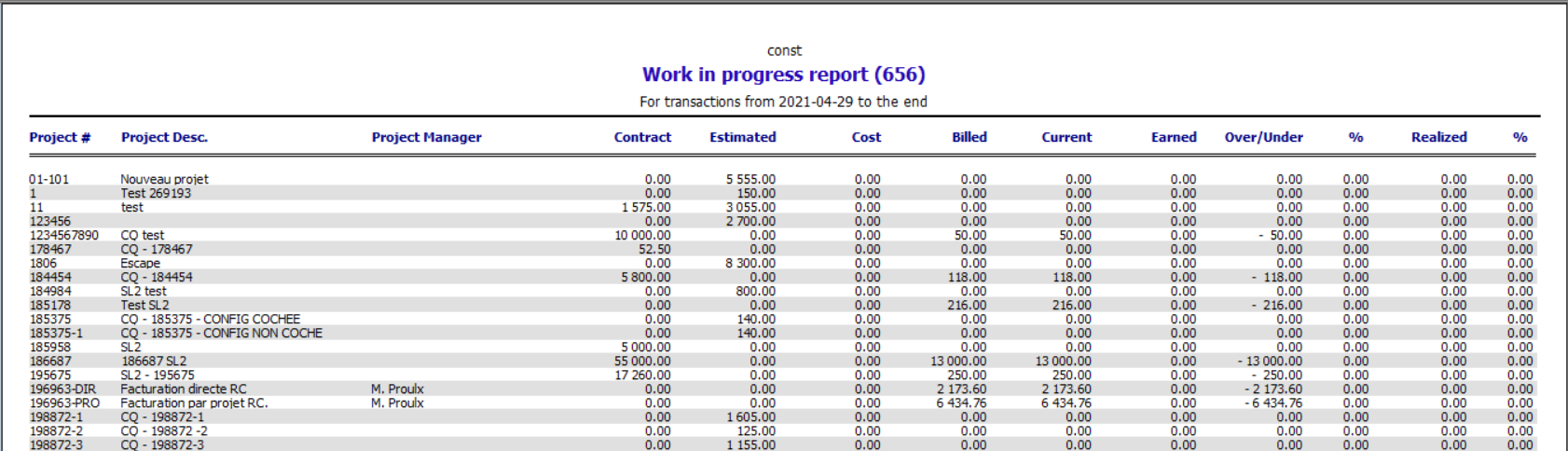

Calculating Works in Progress for a Specific Period

As previously mentionned, maestro* offers works in progress reports to users. Once the parameters are completed and a date range is selected, it becomes possible, by displaying the difference between budgeted and actual project expenditures, to know the value that must appear in the works in progress general ledger account. This provides the user with the data to make the necessary accounting entries.

Below are two examples of maestro* reports that can be used to calculate works in progress for a set period. During the software implementation, other reports, specifically addressing the needs of the customers, can be created. Finally, some customers also choose to use more than one report to perform works in progress calculations; the report used depends on the project type or other characteristics.

As Assets

Conversely, managing works in progress as assets means that expenses are accounted for in asset accounts, according to their nature and the configurations previously set in maestro*. When closing a period, the costs recorded in the assets of projects, for which the end of the work has been indicated, will be automatically reversed to expenditure accounts.

This approach is usually interesting for projets that do not involve progress billing and for whose duration is limited in time, ranging from a couple weeks to a couple months. It is also the approach generally favoured by contractors in residential construction, for which income only arises when a house is sold, whereas the majority of the costs have already been accounted for. The idea is to record expenses in the period in which income arises.

For example, during the contruction of a condo tower (the master project), all units (the projects) will be built, including those that have not yet been sold. If works in progress are managed as assets, the unsold condos will make up a company asset. It will therefore be desirable to record expenditures on units only once they are sold.

Reverse Expenses That Were First Recorded as Assets

When a period is closed in maestro* (such as the end of each month), works in progress of projects for which the project end date falls within the period are reversed and expensed.

In the example above, a project end date will be associated with the project corresponding to the condo once the sale date has been established, so the works in progress amount on the project will be expensed when the period is closed in maestro*.

|

|

Period A financial year is divided in periods for each months of the year. Added to these is a thirteenth period corresponding to the closing of the financial year. Once a period is closed, it is no longer possible to enter transactions on projects contained in the date range of that period. The Projects module uses the periods set in the Accounting module. If a period is closed in the Projects module, the other auxiliaries remain open and use the active period in the general ledger. When closing a period in the Projects module, it is possible to only close the period in this auxiliary. It is therefore possible to still enter transactions in other modules. However, the project periods must be closed in order to be able to close the accounting periods. Periods must be closed following a chronological order. It is possible to close more than one period at a time. Finally, the Reopen a Project Period option makes it possible to reopen a closed period. |

Works in Progress Management Applied to Service

When services are provided by companies (e.g. maintenance contracts, snow removal contracts, etc.), it is common for them to charge customers before the service is provided. They therefore need to manage income received in advance. When the expense is actually incurred or occurs, or is on a regular basis, a portion of the deferred revenue is removed and applied to the financial results of the period in which the expense occurs.

Obviously, if the billing is done after the fact, i.e. after the service has been provided, the costs will first be charged to work in progress and therefore temporarily placed on the assets side of the balance sheet. Once invoiced, a reversal entry will be made to remove the work in progress amount and apply it to the expenses of the current period.

|

|

| maestro* ˃ Projets ˃ Maintenance ˃ Projet ˃ Configurations diverses |

| maestro* ˃ Facturation ˃ Maintenance ˃ Contractuelle ˃ Configurations diverses |

| maestro* ˃ Projets ˃ Maintenance ˃ Projet ˃ Gestion des projets |

| Date fictive | Compte | Nature du compte | Débit | Crédit | Notes |

|---|---|---|---|---|---|

| 2022-03-15 | Travaux en cours | Actif | 8000 | ||

| 2022-03-15 | Compte à payer | Passif | 8000 |

| Date fictive | Compte | Nature du compte | Débit | Crédit | Notes |

|---|---|---|---|---|---|

| 2022-03-31 | Travaux en cours | Actif | 8000 | ||

| 2022-03-31 | Dépense | Dépense | 8000 |

| Date fictive | Compte | Nature du compte | Débit | Crédit | Notes |

|---|---|---|---|---|---|

| 2022-04-01 | Compte à recevoir | Actif | 10 000 | ||

| 2022-04-01 | Travaux en cours | Actif | 8000 | ||

| 2022-04-01 | Bénéfices | Capital | 2000 |

| Date fictive | Compte | Nature du compte | Débit | Crédit | Notes |

|---|---|---|---|---|---|

| 2022-04-01 | Ventes | Revenu | 8000 | ||

| 2022-04-01 | Travaux en cours | Actif | 8000 |

| Comptabilisation des dépenses dans des comptes d'actif (travaux en cours) - Premier mois | |||||

|---|---|---|---|---|---|

| Date fictive | Compte | Nature du compte | Débit | Crédit | Notes |

| 2022-03-15 | Compte à payer | Passif | 5000 | ||

| 2022-03-15 | Travaux en cours | Actif | 5000 | ||

| Production d'une première facture pour le client | |||||

|---|---|---|---|---|---|

| Date fictive | Compte | Nature du compte | Débit | Crédit | Notes |

| 2022-03-31 | Compte à recevoir | Passif | 6500 | ||

| 2022-03-31 | Travaux en cours | Actif | 5000 | ||

| 222-03-31 | Bénéfices | Capital | 1500 | ||

| Comptabilisation des dépenses dans des comptes d'actif (travaux en cours) - Deuxième mois | |||||

|---|---|---|---|---|---|

| Date fictive | Compte | Nature du compte | Débit | Crédit | Notes |

| 2022-04-15 | Compte à payer | Passif | 3000 | ||

| 2022-04-15 | Travaux en cours | Actif | 3000 | ||

| Renversement des travaux en cours vers des comptes de dépenses, une fois le projet terminé et la fermeture de période effectuée | |||||

|---|---|---|---|---|---|

| Date fictive | Compte | Nature du compte | Débit | Crédit | Notes |

| 2022-04-30 | Travaux en cours | Actif | 8000 | ||

| 2022-04-30 | Dépense | Dépense | 8000 | ||

| Production d'une seconde facture pour le client | |||||

|---|---|---|---|---|---|

| Date fictive | Compte | Nature du compte | Débit | Crédit | Notes |

| 2022-04-30 | Compte à recevoir | Passif | 3500 | ||

| 2022-04-30 | Travaux en cours | Actif | 3000 | ||

| Bénéfices | Capital | 500 | |||

| Fermeture du contrat | |||||

|---|---|---|---|---|---|

| Date fictive | Compte | Nature du compte | Débit | Crédit | Notes |

| 2022-04-01 | Ventes | Revenu | 8000 | ||

| 2022-04-01 | Travaux en cours | Actif | 8000 | ||

| maestro* ˃ Projets ˃ Gestion des opérations ˃ Fonctions ˃ Génération des écritures de TEC |

| maestro* ˃ Facturation ˃ Facturation contractuelle ˃ Fonctions ˃ Montants de travaux en cours |