Projections, Budget, and Contingencies

Project management goes hand in hand with risk analysis. Furthermore, there are numerous methods to manage project costs, just as there are many cost variations in the construction industry. Whatever the preferred method is, it is important to keep tabs on projects and their budgets during the progress of the construction work. To this effect, here are the various methods suggested by Maestro and possible with the data generated by the software.

|

|

|

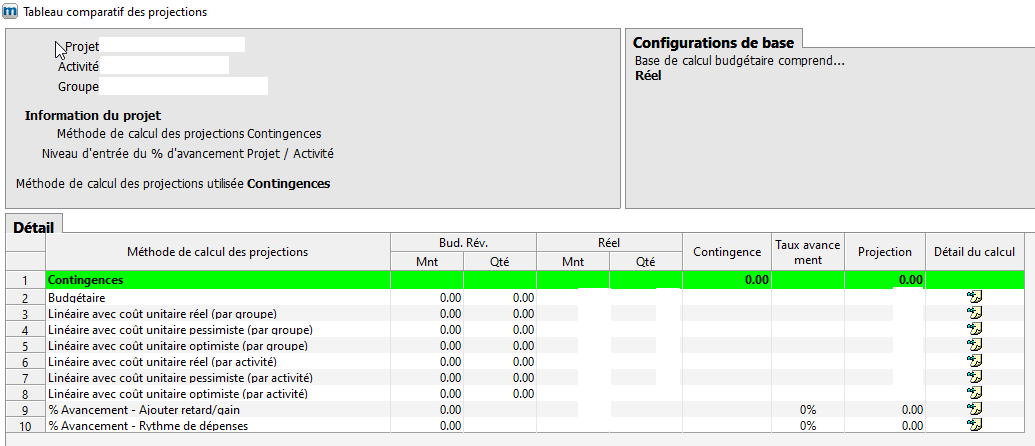

Projection Methods in maestro*

In maestro*, there are a dozen methods available to the user to calculate the final cost (projection) of a project while it is in progress. Some of these methods allow for the follow up of unit costs (most specific to civil engineering or specialist companies) and/or the follow up of lump sums. The method can be selected in the project itself (allowing for an appropriate projection method to be used for the project) or by project types (if project types have been set).

The Contingency Method (Advanced or Not)

While the term contingency refers to risk planning and a means to deal with unforeseen situations, in maestro* it is actually an amount or quantity that is added to a project, by activity or by group. This amount or quantity is then used to perform calculations and make a projection for the project.

The Budget Method

The budget method simply asks of a user to look at the projects to analyze whether the committed costs are greater or less than those planned, and if the financial projections still correspond to the initial budget. That way, if the actual costs plus the committed costs equal less than the initial budget, the projection equals the budget. If, however, the actual costs plus the committed costs equal more than the initial budget, the projection then equals the sum of the real and committed costs.

The Linear Methods

To calculate a projection, the various linear methods consist of determining a unit cost for the produced quantities and applying this cost to the remaining quantities to be received to complete the project.

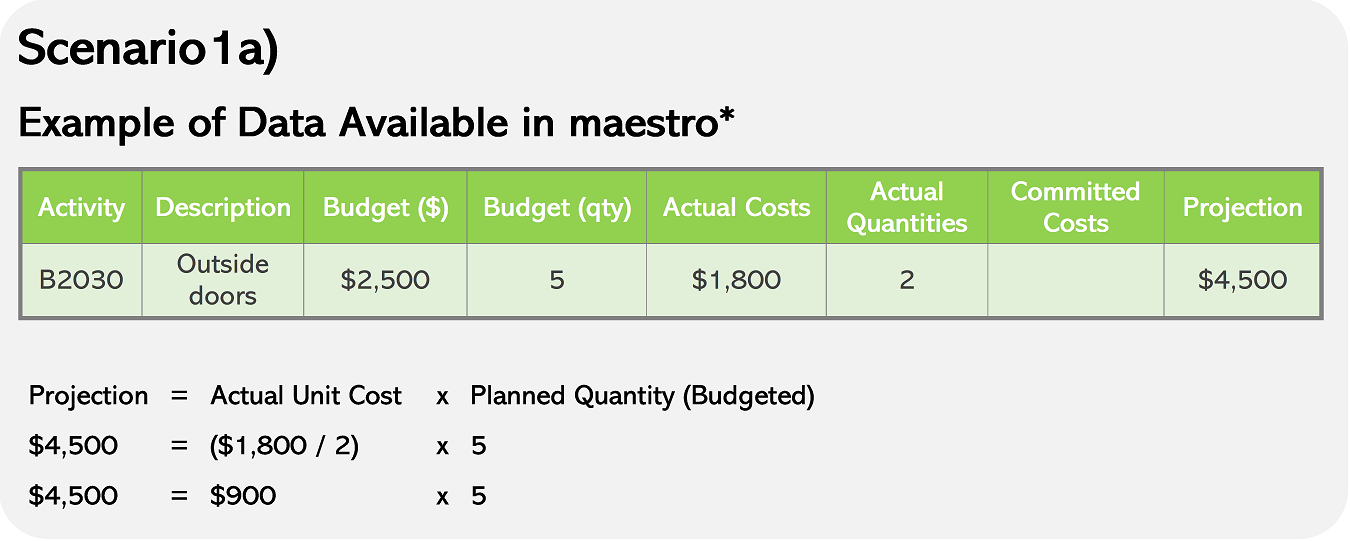

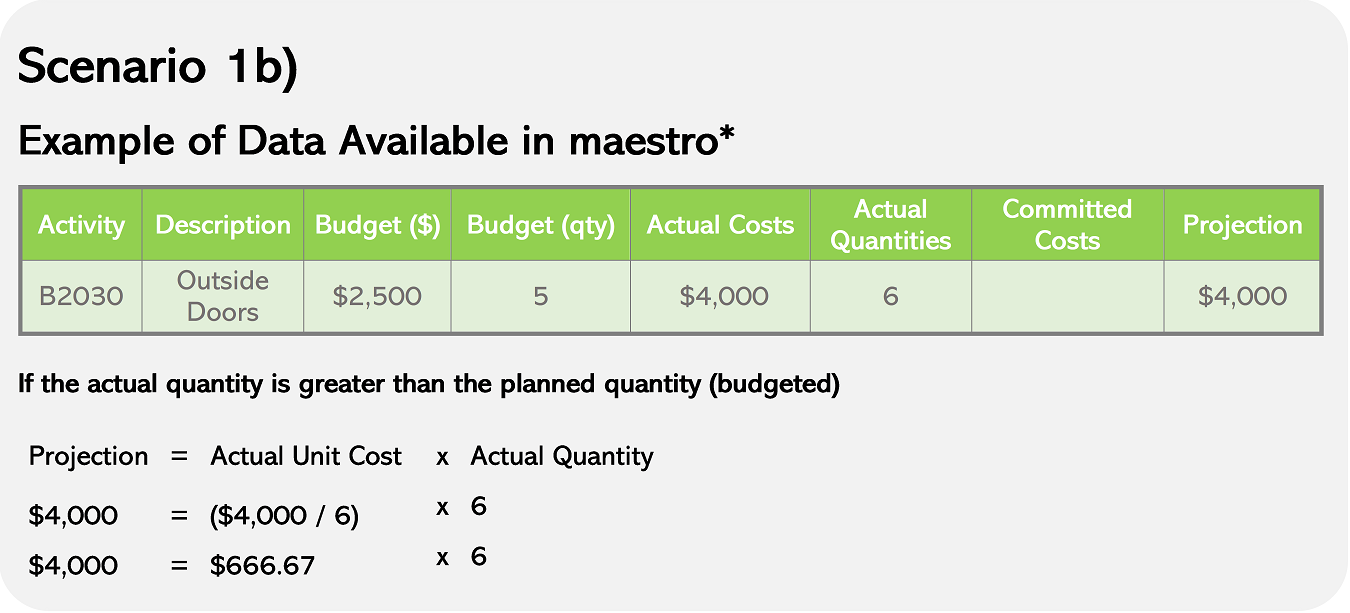

Linear Method with Actual Unit Costs - By Group

Making a projection with this method simply asks that you multiply the actual unit cost, on the reevaluation date, by the planned quantity (budgeted). However, if the actual quantity is greater than the planned one (budgeted), it is the actual quantity that is used to calculate the projection.

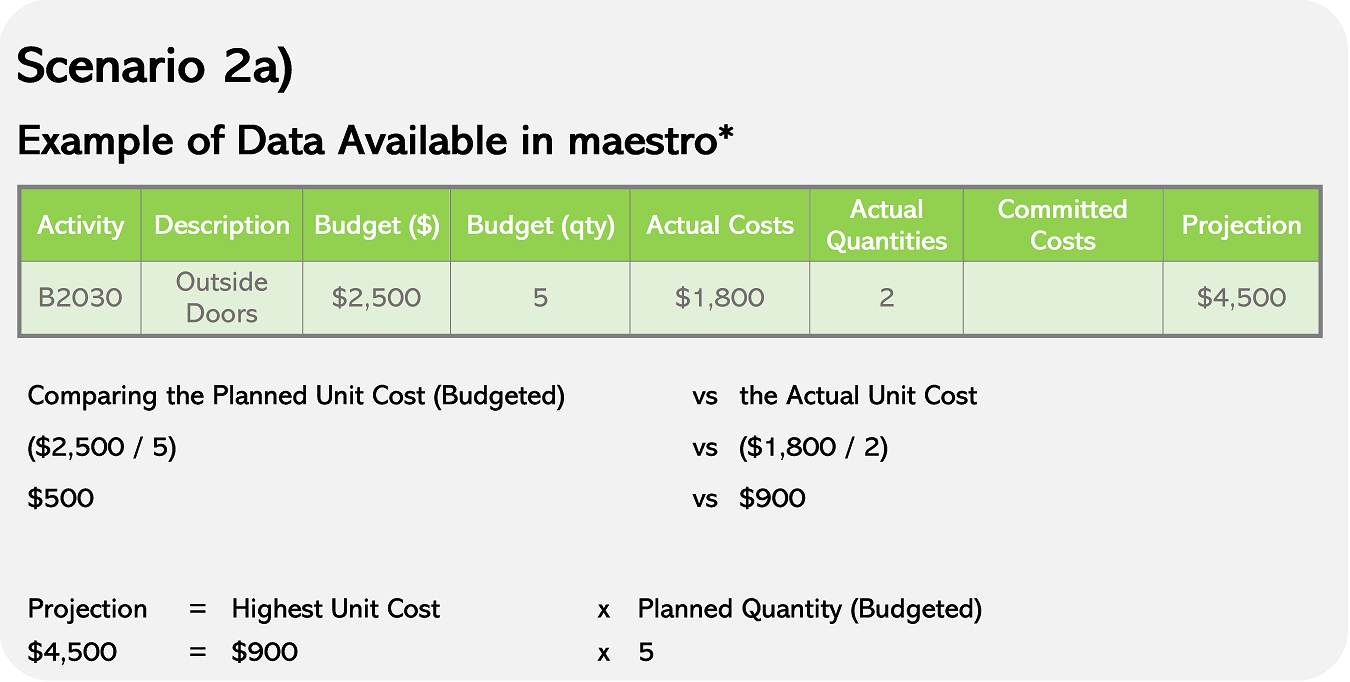

Linear Method with Pessimistic Unit Costs - By Group

This projection method is based off the comparison of the planned unit cost (budgeted) to the real unit cost. If the actual unit cost is greater than the planned unit cost (budgeted), then it is the actual unit cost that is multiplied by the planned quantity (budgeted). If, however, the actual unit cost is less than the planned one, it is the planned unit cost (budgeted) that will be multiplied by the planned quantity (budgeted). And in order to get a glimpse of the worst case scenario, the planned quantity (budgeted) is replaced by the actual quantity, if the latter is greater.

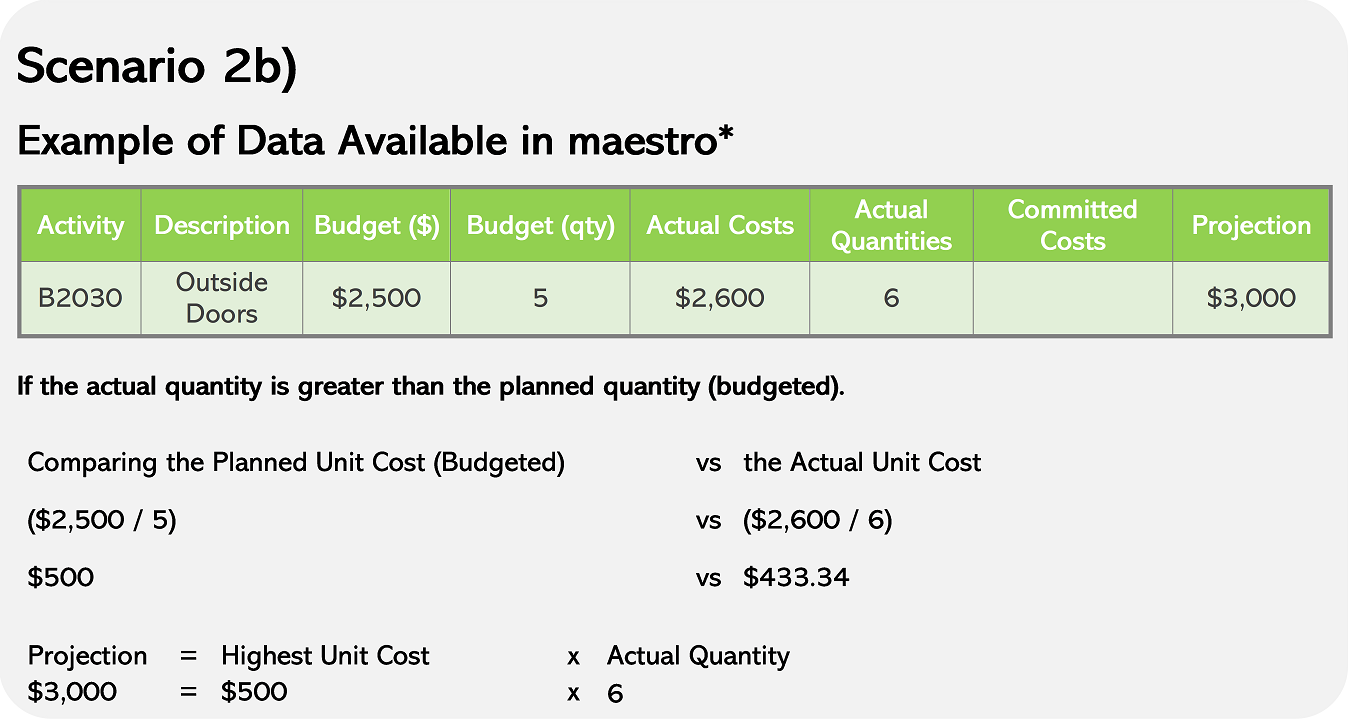

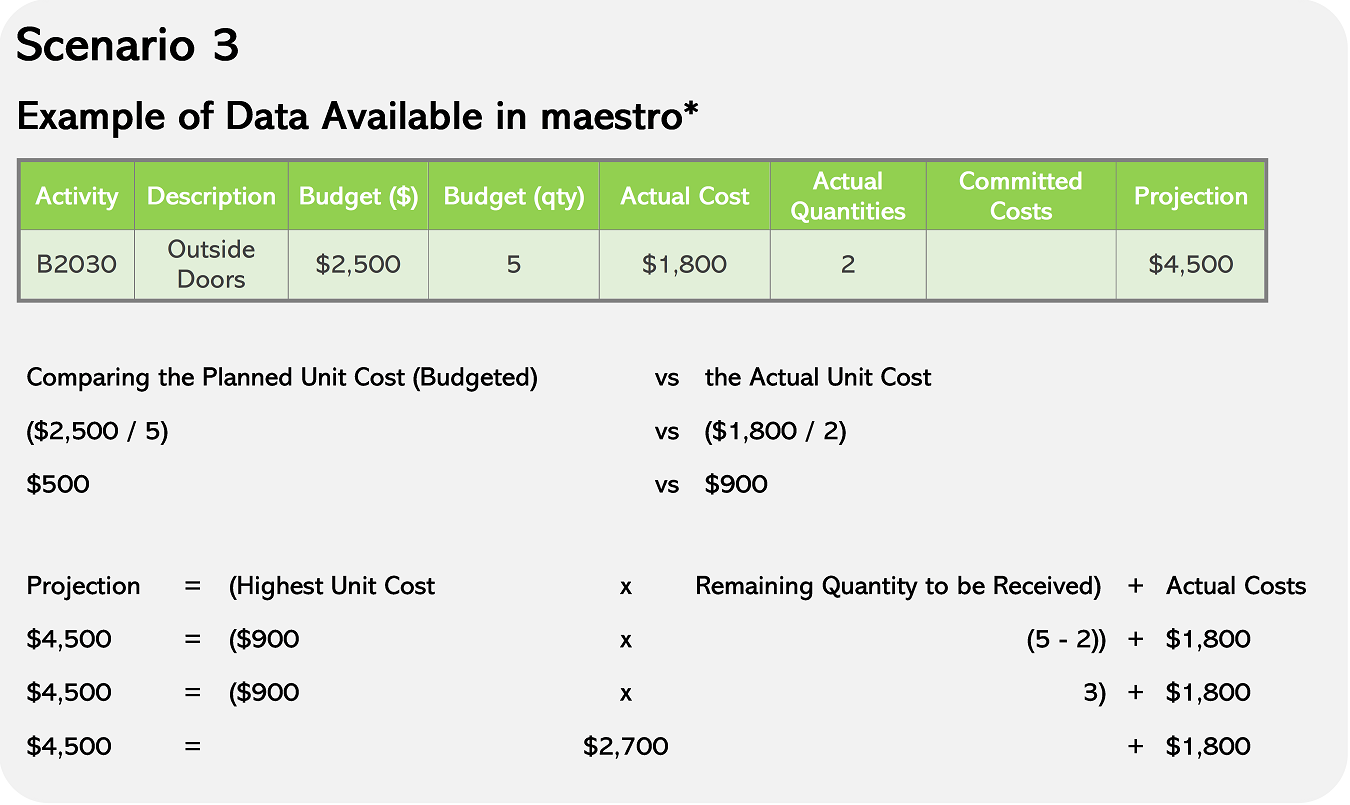

Linear Method with Optimistic Unit Costs - By Group

This projection method is also based on the comparison of the planned unit cost (budgeted) to the actual unit cost.

To perform the necessary calculations of the linear projection method with optimistic unit cost, it is mandatory to use the highest unit price (between the actua; unit cost and the planned unit cost (budgeted)) and to multiply it by the remaining quantity to be received (the planned quantity minus the quantity received to date). To this must be added the sum of expenses to date for the acquired quantity.

|

|

The three methods that follow, the activity-based methods, are identical to the group-based methods, with the only exception that the planned quantities (budgeted) correspond to the quantities to be received and the actual quantities come from the maestro* Production option. |

Linear Method with Actual Unit Costs - By Activity

Making a projection using this method simply consists of multiplying, for the activity, the actual unit cost by the quantity to be produced. However, if the actual quantity, which comes from the Production, is greater than the quantity to be produced, the actual quantity is used to calculate the projection.

Linear Method with Pessimistic Unit Costs - By Activity

This projection method is based on the comparison of the planned unit price (budgeted) to the actual unit cost. If the actual unit cost is higher than the planned unit cost (budgeted), the actual unit cost is multiplied by the quantity to be produced. Otherwise, if the actual unit cost is less than the planned one, the planned unit cost (budgeted) will be multiplied by the quantity to be produced. And in order to get a glimpse of the worst case scenario, the quantity to be produced is replaced by the quantity in the Production option, if it happens to be greater than the former. In sum, this scenario suggests the use of the higher unit cost and the greatest quantity to calculate the projection.

Linear Method with Optimistic Unit Costs - By Activity

This projection method is based on the comparison of the planned unit cost (budgeted) to the actual unit cost.

To perform the necessary calculations of the linear projection method with optimistic unit cost, it is mandatory to use the highest unit price (between the actual unit cost and the planned unit cost (budgeted)) and to multiply it by the remaining quantity to be produced (the planned quantity minus the quantity received to date). To this must be added the sum of expenses to date for the received quantity.

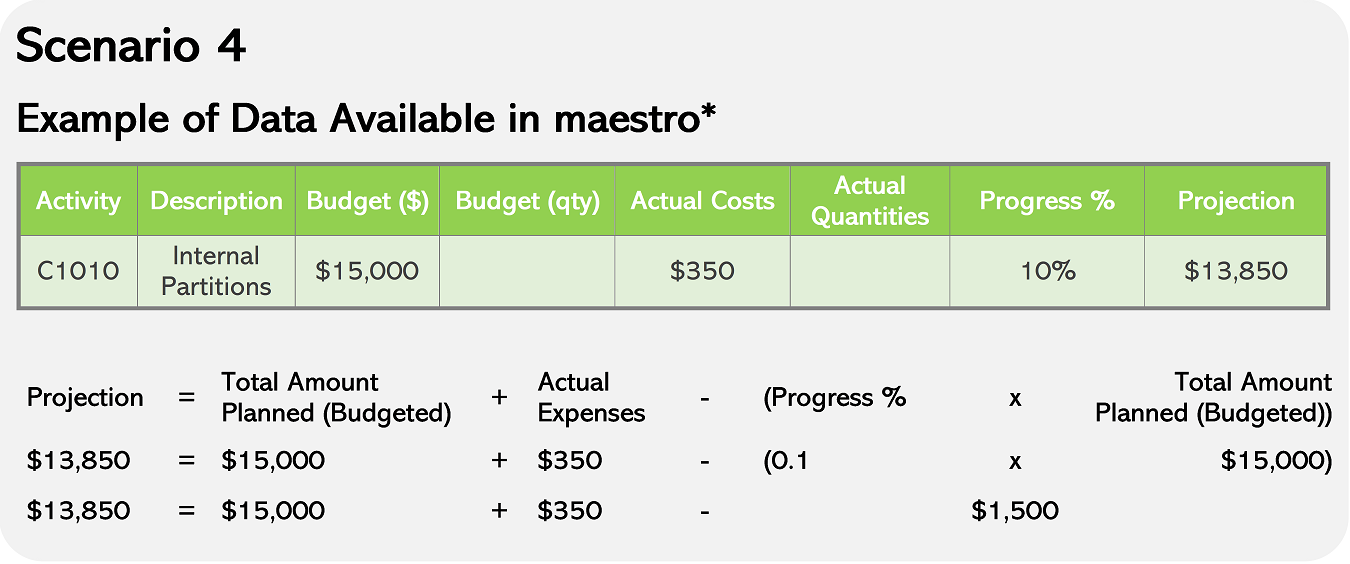

Progress Percentage Method - Addition of Delays/Gains

This projection method calls upon the progress percentage entered by the user in the Project Progress option to calculate the loss or gain.

The calculation's formula is the following:

Projection = Total Amount Planned (Budgeted) + Actual Expenses - (Progress % x Total Amount Planned (Budgeted))

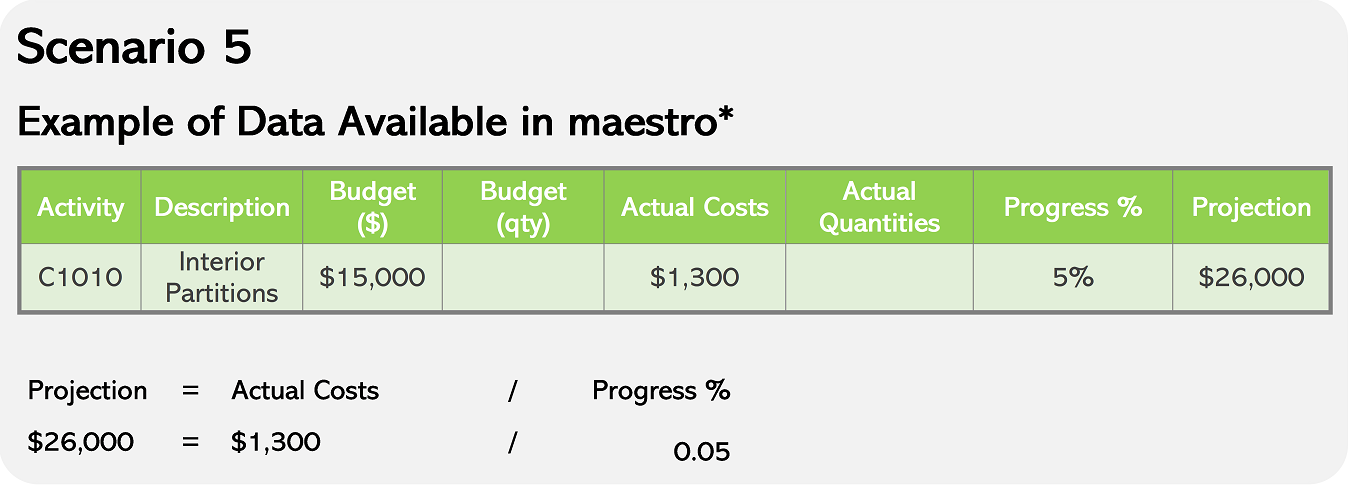

Progress Percentage Method - Expense Rate

This method involves dividing the real expenses by the work progress percentage, i.e. :

Projection = Actual Costs / Progress %

|

|

If most of the expenses are made at the beginning of the project, rather than as the goes on, this can lead to a disproportionate projection. |

Summary of the Different Methods

|

|

|

|||||||

|---|---|---|---|---|---|---|---|---|

|

|

Requires a monthly input of contingencies (either amounts or quantities) so that maestro* can then calculate a projection for that project. |

|||||||

|

|

Is the comparison between actual and budgeted costs. |

|||||||

|

|

||||||||

|

|

|

|||||||

|

|

|

|||||||

|

|

||||||||

|

|

Calculation which takes into account the total budgeted amount, the progress percentage, and the actual expenses. |

|||||||

|

|

Calculation based on the actual expenses and the progress percentage. |

|||||||

|

|

Maestro* allows to see at a glance the summary results of each of the PAG (project-activity-group) projection calculation methods in the Project Inquiry option. |

|

|