Equipment Management and Finance Processes

Whether it be a piece of equipment or a machine, maestro* grasps all material that can be used for a project. Tools, heavy equipment, fabrication tools, and company vehicles; all can be considered as equipment, whether they belong to the company or are rented.

|

|

Project Costs Allocation

Since the use of equipment is preponderant in most construction projects and companies, it is important for its use to be reported and to know its financial impact. The allocation of costs to construction projects, such as those linked to the use of equipment, makes it possible to know the actual project costs. However, it is important to understand and validate them. To evaluate whether the equipment's hourly rate is reasonable, Maestro recommends the creation of a project for each piece of equipment and to charge the usage income to the respective project. If, for example, the equipment project turns out to be very profitable, it could possibly indicate that the hourly usage rate is too high, and/or that the construction project costs are overestimated. Conversely, if the equipment project is in deficit, this could mean that the equipment is not used at its fullest, and/or that we overvalued the construction projects' profitability by funding them with hourly usage rates that were too low.

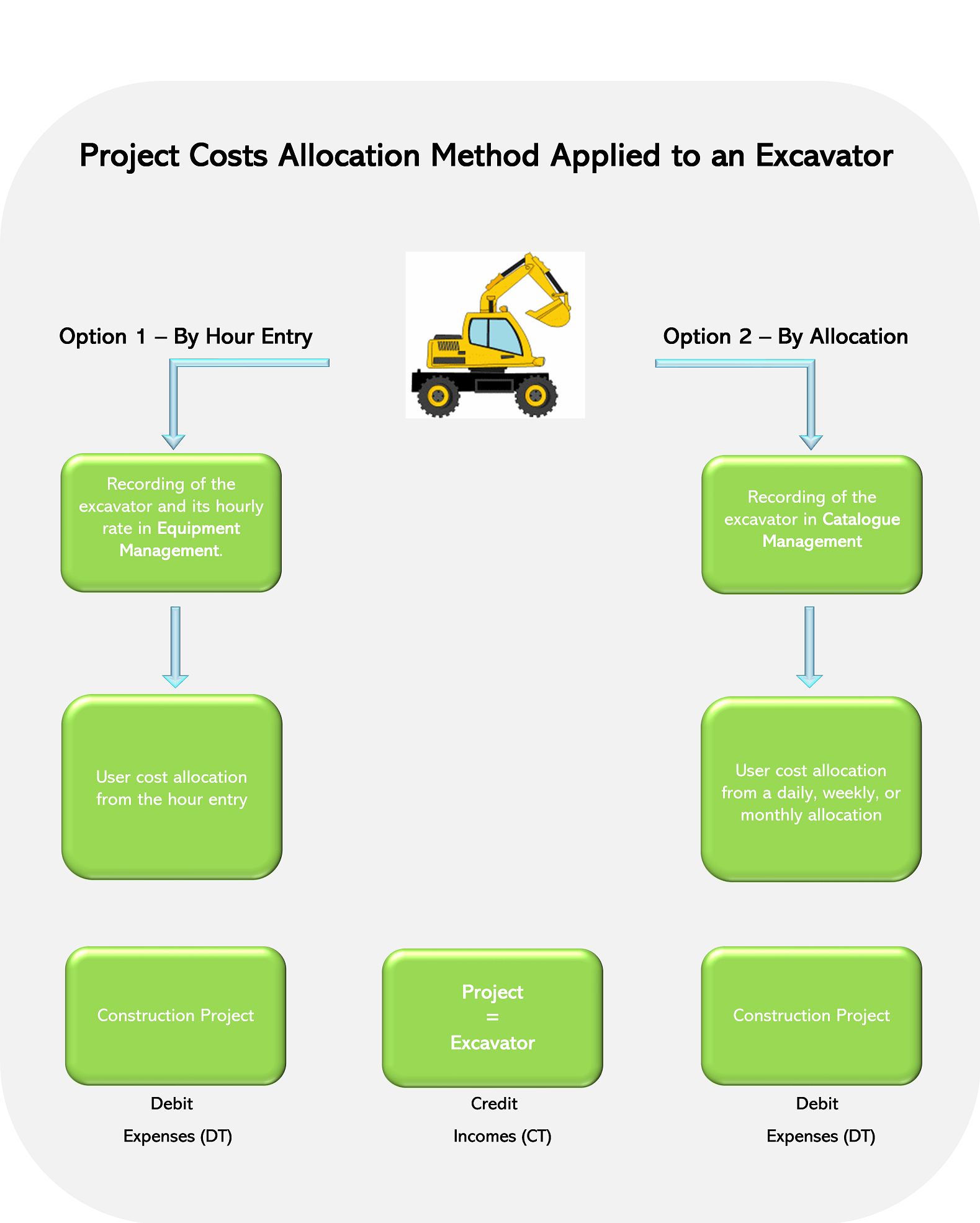

There are usually two methods used to charge the use of equipment t construction projects: entering the hours of use and allocations.

By Hour Entry

In the various worked hours entry methods in maestro*, it is possible to specify if pieces of equipment were used, and for how long. This makes it possible, is part, to associate equipment and tool usage costs to the project, and thus, get more accurate project costs.

To do so, maestro* allows the allocation of four hourly rates for the use of each piece of equipment configured in maestro*; these latter being identified with the help of a code. The first rate generally represents the use of the equipment alone, whereas the others might include, for example, the use of gas and/or more users. A company could, for example, define the following rates for the use their equipment:

The rate can be selected when entering the number of hours of use. Better yet, it can be chosen upon the creation of the construction project in maestro*. Thus, for a long-term project that uses a lot of machinery, a company can prefer to account for gasoline as an expense, and directly apply it to the construction project. In this example, the rate, selected by default, for the construction project and selected equipment, consists of the use of equipment rate only. If, on the contrary, the equipment is used for various projects, the preferred rate will be with operators and gas, for those projects. The same logic applies if there is allocation, or not, of an operator, or of all other costs to a piece of equipment.

This method is usually used to apply large equipment, heavy machinery and/or vehicle usage costs to construction projects.

By Advanced Allocation

Another way of doing consists of listing the equipment, or a part of them, in the maestro* catalogue, and then set a daily, weekly, or monthly allocation. Recurring equipment usage costs will be applied to the designated construction project and, in return, an allocation will be systematically paid to the project linked to the equipment used. This method is often preferred to apply small tool usage costs, or when a piece of equipment is used long-term on a project.

Equipment and Profit Centre

As previously mentioned in the chapter on profit and cost centres, the equipment project can be considered as a cost centre. However, it is possible, and recommended, to make sure that it becomes a profit centre by applying an income to the equipment project, generated by the use of equipment on construction projects. Indeed, the fees charged to construction projects for the use of equipment can translate into income that counterbalances the equation and makes it possible for the equipment project to become a profit centre. This also makes it possible to monitor its profitability. This profit centre can be limited to the one equipment project, or it can regroup many projects of a common nature or trait (generators, parking), according to the business's analysis needs.

Whether the company owns or rents the equipment, the costs must be considered and applied to the profit centre:

- Maintenance

-

-

-

-

-

-

-

-

- Etc.

Equipment Management Options

There are several ways to manage equipment and monitor their profitability in maestro*. Only one method can be used, but it is also possible to use more than one, depending on the quantity of equipment, their characteristics, the available information coming from the construction site, and the wants/needs of the company.

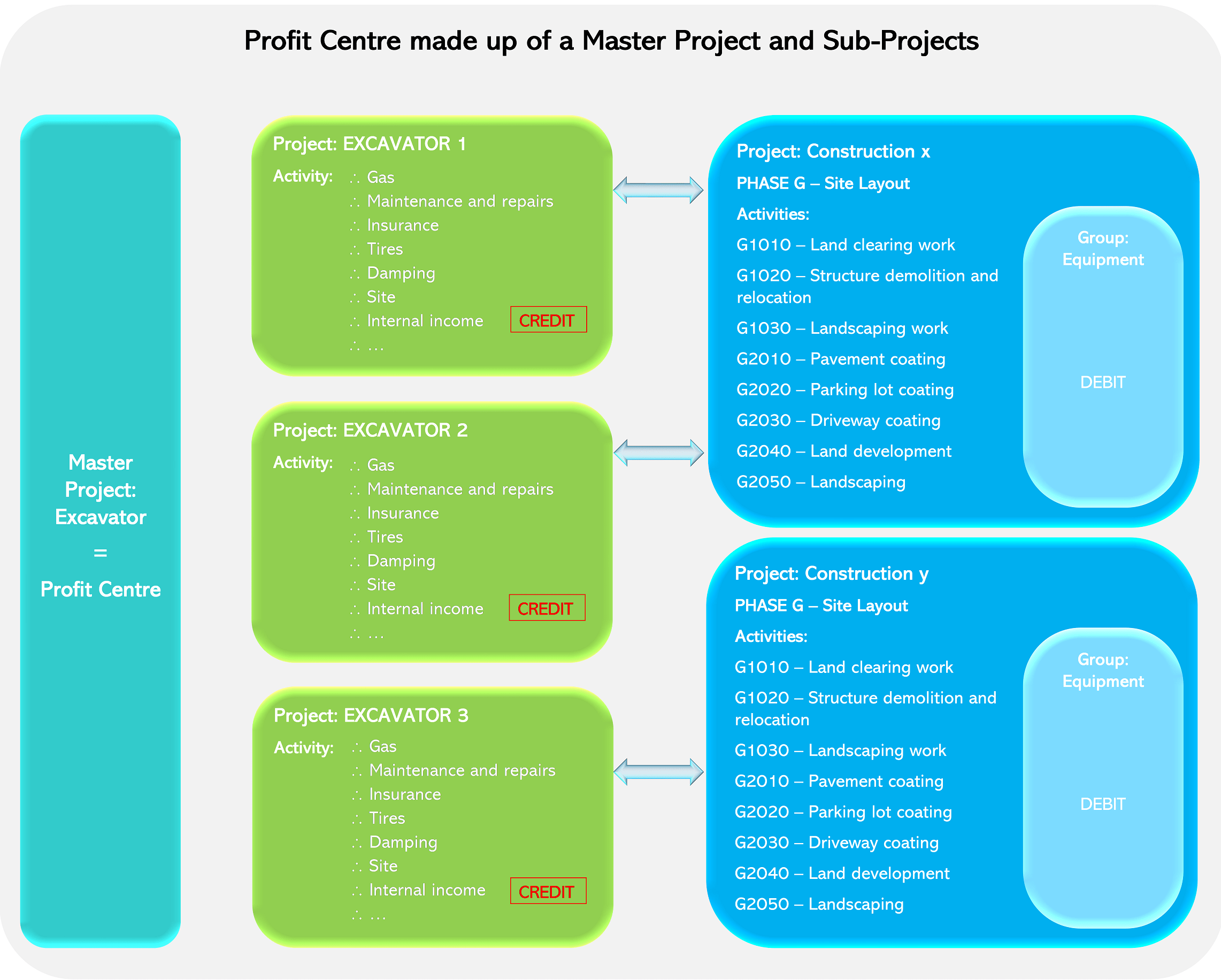

Option A

Creating a Profit Centre made up of a Master Project and Sub-Projects

Large equipment and/or equipment of the same nature can be managed as a profit centre; each equipment, in itself, makes up a sub-project, and the set of equipment sub-projects is overseen by a master project, which regroups all sub-projects. An identical project structure is used for each sub-project (equipment), and expense and income activities are displayed there. There are activities for usage fees, such as repairs, maintenance, damping, etc., as well as a usage income activity, that which provides the accounting counterpart of usage charges, the former being applied to construction projects through the entrance of hours.

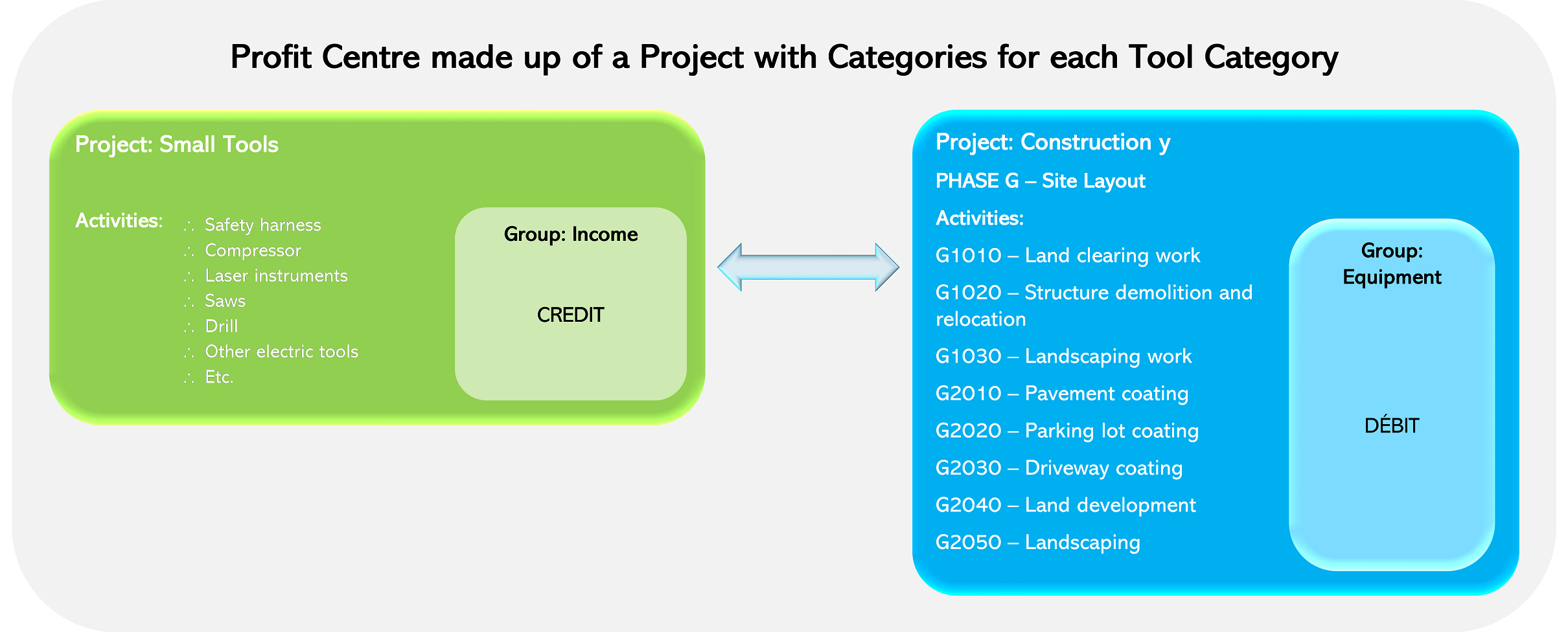

Option B

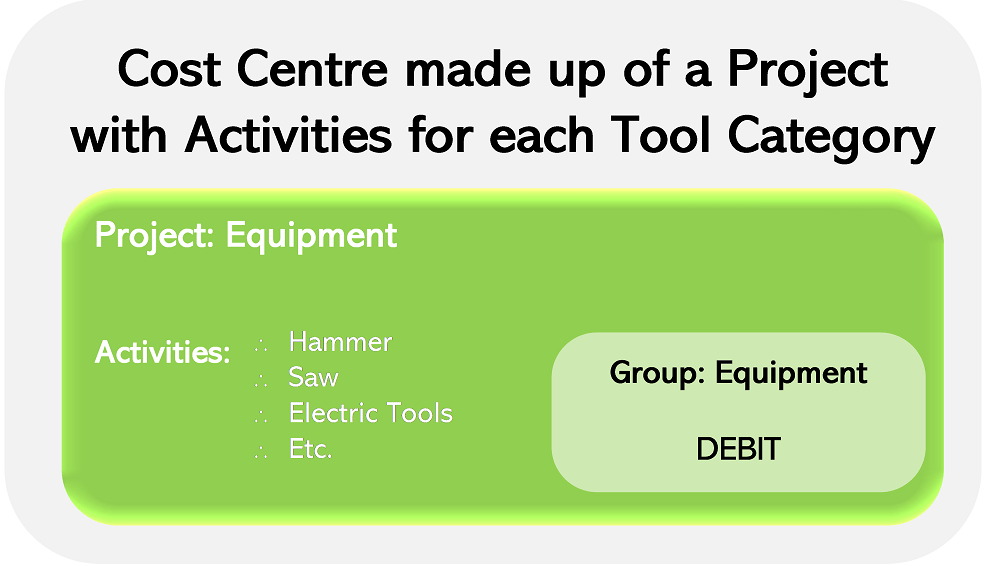

Creating a Profit Centre made up of a Project with Activities for each Tool Category

This option advocates for the creation of a project, for all equipment, and the creation of activities for each major equipment category. This is a common way of managing small tools since the creation of a distinct project for each of them would make it more complex. This method also makes the project a profit centre; the usage costs are charged to the construction projects and, as for the corresponding incomes, they are allocated to the project created for the equipment. Two options are offered to the user concerning the allocation of usage expanses to construction projects:

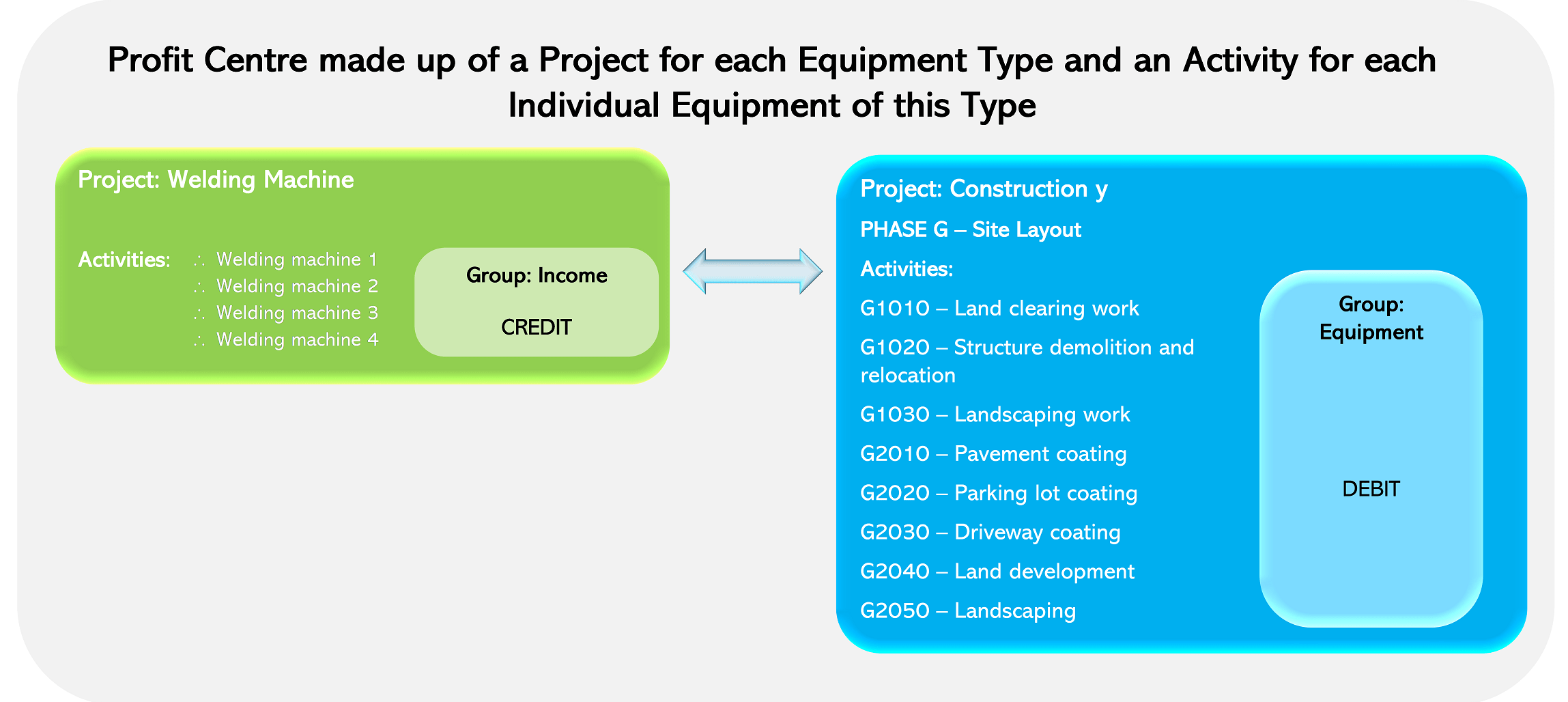

Option C

Creating a Profit Centre made up of a Project for each Equipment Type and an Activity for each Individual Equipment of this Type

Option C proposes a method inspired by the previous two. A project is created for each equipment type, which makes it possible to benefit from a global portrait of this equipment type, then an activity is associated to each equipment individually, allowing a very close follow-up. This method also makes the project a profit centre; usage costs are charged to construction projects, and, as for the corresponding incomes, they will be allocated to the specific equipment project and activity used.

Option D

Creating a Cost Centre made up of a Project with Activities for each Tool Category

This method implies that equipment usage costs are not applied to construction projects, but instead regrouped to create a general company expense.

Advantages and disadvantages of these options

|

Option |

Description |

|

|

|---|---|---|---|

|

A |

|

|

|

|

B1 |

|

|

|

|

B2 |

|

|

|

|

C |

|

|

|

|

D |

|

|

|

Lastly, companies that own the Preventive Maintenance module (which allows, in part, to plan maintenance according to the number of hours or kilometres used and notify the user when maintenance is required) will be able to generate work orders from the equipment. These work orders will, afterwards, be charged to the applicable profit centre.

|

|

|

o |

|

|

o |

|

|

o |

|

|

o |

|

|

o |

|

|

o |

|

|

o |

|

|

o |

|

|

o |

|

|

o |

|